The Vehicle Sales Authority (VSA) would like to share some important updates with you. Please take a moment to review the information below.

At its December 13 meeting, the Board of Directors approved the VSA’s budget for the next fiscal year beginning April 1, 2024, and ending March 31, 2025, with no fee increases.

Due to labour market conditions resulting in the delayed/late hiring of some VSA staff, along with higher-than-expected new salespersons coming into the industry, the VSA anticipates a surplus budget this fiscal year ending March 31, 2024. The VSA will be using these anticipated retained earnings in next years’ budget allowing for no fee increases.

Ken Affleck, KC, Registrar, has determined that the annual $300 contribution to the Compensation Fund can be waived for the coming fiscal year. This waiver does not apply to new dealers who have not yet paid their legally required $300 contribution for each of the first three years of their operations.

As at November 30, 2023, the Compensation Fund balance was $1,126,472.00. As at November 30, 2022, the Fund Balance was $1,111,644.00. The increase in the balance was due to prudent management of the Fund, and contributions from new dealers who are legally required to pay $300 a year into the Fund for the first three years of their operations. The Registrar has set a minimum reserve for the Fund of $1 million, which an actuarial report in 2022 indicates is a sufficient reserve amount.

It has come to the VSA’s attention that some dealers who require consumers to finance their purchases are having the consumers agree to pay the dealer a certain amount of money, should the consumer pay off the outstanding amount owing before the end of the agreement. This practice is illegal in B.C.

Under section 74 of the Business Practices and Consumer Protection Act (BPCPA), a consumer has the right to repay a credit grantor (this includes: banks, credit unions, leasing companies, other financial institutions, anyone who advanced the consumer credit including the dealer if the dealer advanced the credit) the full amount owing at anytime and the consumer cannot be charged a prepayment charge or penalty for doing so. The consumer cannot waive or release this right by an agreement: section 3 of the BPCPA. A dealer representing to a consumer, verbally or in writing, that the consumer must pay the dealer an amount of money should the consumer payoff their credit agreement too soon, will have committed a deceptive act or practice contrary to section 5 of the BPCPA, as deemed by section 4(3)(b)(iv) of the BPCPA.

The Registrar is empowered to administer sections, 4, 5 and 74 of the BPCPA. It is important to note that section 8.1(4)(b) of the Motor Dealer Act says a breach of these provisions by a motor dealer is grounds for the Registrar to consider that is not in the public interest for the motor dealer to be registered or continue to be registered, and the Registrar may suspend or cancel the motor dealer’s registration. The Registrar assesses this on a case-by-case basis.

Deceptive acts or practices, failure to disclose material facts, failure to act with honesty and integrity, failure to include required information, offsite sales, unlicensed salespeople, breaching the Code of Conduct, and failing to disclose information when entering into a distance sale.

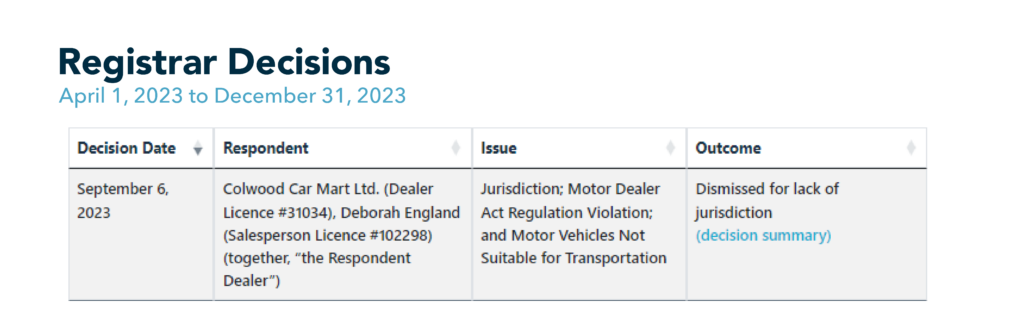

All formal compliance activities are posted on the VSA website within seven days of the decision date. Previous compliance activity reports are also available on the VSA website and may be a useful tool for dealers to evaluate their current business practices.

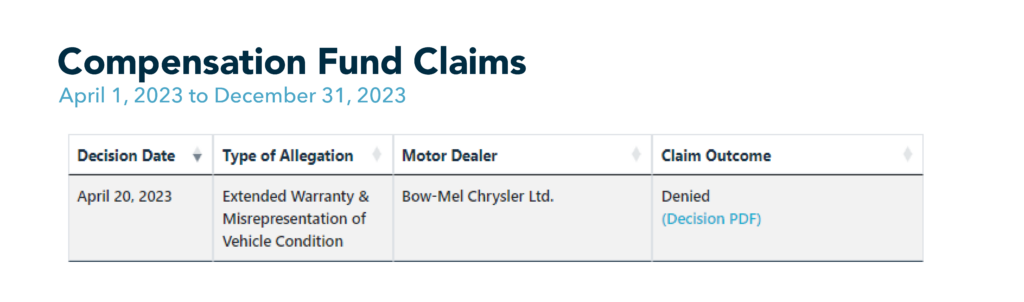

The Compensation Fund Board denied one claim in this period. This claim involved extended warranty & misrepresentation of vehicle condition.